Health Insurance for Seafarers

Overview

- You must have heard of various health Insurance companies like Star Health Insurance, Care Health Insurance, Aditya Birla Health Insurance, etc. Have you ever wondered what it truly means and what the benefits of Health insurance are?

- In this Blog, we are going to answer some of the critical questions relating to Health Insurance and try to impart as much knowledge as possible to help you make an Informed Decision.

- This Blog will help you realize the importance of Health insurance in the Merchant Navy and the correct ways to go about buying one.

- Check out the top 3 insurances a Seafarer must have to sail smoothly without worrying about the family and future.

1:- What is Health Insurance?

- ‘The high medical inflation in India in 2022 increased retail premiums by 16.5% and group health insurance premiums by 31%. Despite this, demand for medical insurance saw an overall rise of 25% in 2022 ’-TATA AIA.

- Minor Surgeries and Hospitalization in recent times can cost you a lot of money. Forget about the Major Ones!

- To Safeguard your Financial stability during a medical emergency or hospitalization, Health insurance provides a guarantee of financial support or reimbursement.

- Health Insurance premium is the money charged by the insurance company to provide the financial guarantee of the covered amount to the buyer.

2:- Benefits of Health Insurance for Seafarers

A correct Health Insurance policy can help smoothen your life in a lot of ways.

Here are some of them:

- Better Financial Security and Flexibility –

With the proper health insurance, you do not need to worry about saving up for a medical emergency and focus your resources on other financial assets

- Peace of Mind

In case of an Emergency, you may be psychologically hurt but you will not have to worry about the money. Less worry in general leads to better productivity.

- Access to better medical facilities

Good Health Insurance policies cover major hospitals in your city. You may opt for a good hospital because you do not have to worry about the money. Good Hospitals also try to smoothen your insurance claim.

- Customization

Nowadays, Health Insurance policies can be customized according to your personal needs. Based on your specific demands a health insurance policy can be modified

- Relatively Low Premium

If considering the financial and psychological stress incurred during a medical emergency, premiums will seem cheaper.

- Saved Assets and Investments

We invest so that our money grows with time. Untimely financial need like a medical emergency may cripple your investments if you are not financially prepared.

- Better Health Habits

Some people tend to develop better health habits to avoid paying extra premiums. Ironic isn’t it?

- Tax Benefits

Section 80D allows a tax deduction of up to Rs 25,000 per financial year on medical insurance premiums. Section 80D also includes a Rs 5,000 deduction for any expenses paid for preventative health check-ups.

Several other benefits of health insurance lie in the various features a health Insurance policy may offer.

Check out complete information about Health Insurance for seafarers with our dedicated course on Insurance for Seafarers.

3:- Features of Health Insurance

Some of the salient features of Health Insurance Policies are stated below. These are some of the features of health insurance that you should particularly look for.

- Hospitalization Expenses

Most Health Insurance plans cover the expenses of hospitalization, both Accidental and Illness-related. These may include; Room charges, Intensive care unit (ICU) charges, Doctors’ fees, Diagnostic test costs, and Surgery charges

- Pre and Post-Hospitalization Expenses

Health Insurance plans may pay for the expenses incurred before and after the hospitalization takes place. A fixed number of days is determined from when the expenses are calculated, say 30-90 days. These may include expenses such as transportation costs, follow-up visits, medicine, and diagnostic tests,

- Annual Health Checkups

Most Health insurance companies provide the facility for at least one free health checkup for the people insured under the policy. This is particularly important for you as well as the insurance company

- Day-Care Expenses

Some minor treatments do not require even a single night of hospitalization. Some Health insurance companies may also cover these types of expenses.

- Domiciliary Treatments

Doctors may recommend home treatment depending on factors such as the health condition of the patient, unavailability of beds, etc. In such cases, health insurance may provide for the expenses of a home-based treatment.

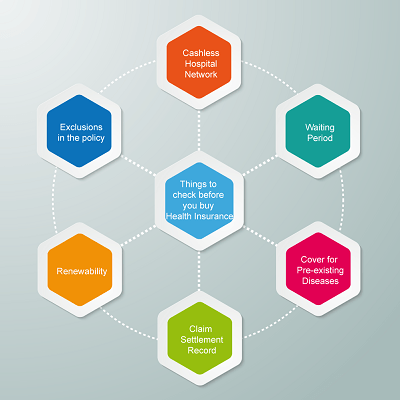

- Coverage for Pre-Existing Diseases

Some insurance companies may cover existing diseases with the application of a waiting period on the policy.

- Cashless Hospitalization

With this feature, you may not have to pay a single dime in cash directly to the hospital. You just have to inform the insurer 48 hours before hospitalization or within 72 hours in case of an emergency

- Add-ons

Many Policies allow the additional cover of a Critical illness add-on to get enhanced coverage on critical illnesses like kidney failure, stroke, heart attack, etc.

- No Claim Bonus

Many companies provide a bonus either in the form of an increased sum assured or reduced premium in case the insured does not claim the policy in a year. This is generally accounted for every year

The more is the NCB, the better it is for your premiums.

- Waiting Period

This is the period that one might have to wait before being able to claim on the policy. During this period, the company will not accept any claims including planned hospitalizations and emergencies, except accidents.

The lesser is the Waiting period, The better is the policy

- AYUSH treatment

Expenses for in-patient treatment under Ayurveda, Unani, Siddha, and Homeopathy (AYUSH) treatment may be covered by a suitable health insurance policy.

- Lifelong renewability

Provision to renew the policy without any restriction of age is also an important feature a good health insurance plan should have.

- Co-Payment

Co-payment is a feature where you decide that when claiming the policy, some portion of it will be paid by you and the rest will paid by the company. This may reduce the premium by the percentage you wish to take as a co-payment.

- Room-rent Sublimit/ Category

Some policies have a limit on the room rent. This will include everything including doctor’s fees, nursing charges, etc. Say there is a room rent limit of ₹5000 and you opt for a room of ₹7000. The balance of ₹2000 will have to be paid by you.

In other cases, there may be a restriction on choosing a room category, like Single Private room, Twin Sharing room only, etc.

- Restoration Benefit

Restoration benefit is an add-on feature that provides an additional sum insured amount once the original sum insured has been exhausted. It comes in handy for individuals with recurring medical expenses.

For example, the policyholder has a sum insured of Rs 10,00,000 and has utilized the entire amount in a policy year. The restoration benefit will automatically restore the sum insured amount for the same policy year, allowing the policyholder to go for further treatments

4:- Mistakes to Avoid While Buying Health Insurance

Buying Health Insurance can be very complicated and as exhausting as a PSC Inspection onboard. There might be some hidden clauses that you should be aware of so that your claim experience is good when the policy will be of utmost need.

These are some of the major mistakes that we make while choosing health insurance and should be aware of:

4.1:- Opting for a Co-payment Option

Ideally, there should be no co-payment clause as it might be troublesome for you as you have to pay a hefty amount from your pocket during times of crisis.

4.2:- Opting for Zonal Co-Payment

There might be a clause that says that if you get treatment outside a specific area mentioned in the policy, you might have to share payment with the company. You should avoid such clauses.

4.3:- Ignoring the Waiting Period Clause

It is safe to avoid policies that have higher waiting periods for current policies, pre-existing illnesses, or illnesses that do not require emergency treatments. Ideally, the waiting period should be as low as possible

4.4:- Room Rent Capping.

It is best to choose a health insurance policy that has no restriction on room rent as it might lead to you spilling out money from your pocket.

4.5:- Choosing No Claim Bonus Instead of an Increase in Sum Assured

In case of no claims in a policy year, the insurance companies may provide a no-claim bonus. It is best to get this in the form of an increase in the sum assured due to increasing medical expenses.

In most policies, the sum assured can be doubled in case of a long stretch of no claims at the cost of the same premium.

4.6:- Ignoring the Sub-Limit on Diseases

Some policies might have a clause saying that they will pay only 50% of the total bill in case of a certain disease, say cardiovascular disease. The rest of the 50% will have to be paid out of your pocket.

Policies with no sub-limit on diseases should be chosen to avoid future hassles.

4.7:- Not Opting for Restoration Benefits

What if you have already exhausted your claim and need further financial assistance in your treatment? Restoration benefits should always be present in your policy to help you avoid such cases.

4.8:- Not Covering Pre and Post-Hospitalization Charges

These expenses are often ignored and people end up paying a hefty amount of money out of their pockets. Always choose policies that cover at least 30 and 60 days of pre-hospitalization charges respectively.

4.9:- Not Opting for a Cashless Facility

A cashless treatment feature comes in handy if you inform the insurance company about a planned hospitalization or an emergency. If the Bill amount is large, you may be in trouble at times.

4.10:- Not Checking the Hospitals Covered

This is of utmost importance as the hospitals of your choice and reach may not be covered under the policy. It is prudent to check if the major and good hospitals are covered in your policy.

5:- What is Family Floater Health Insurance

- A Family floater health insurance plan refers to a plan that covers the entire family of an individual under a single policy.

- Any of the insured family members can utilize the same sum assured, The sum assured is exhaustive after a claim is made.

- For Example, Mr. X takes a family floater insurance plan for Rs. 10 Lakhs. The people insured under the policy are his wife, himself, and his kids. All of them put together will be covered for 10 Lakhs. If Mr. X gets hospitalized and claims Rs. 5 Lakhs from the policy, the plan now has a coverage of Rs. 5 Lakhs for the entire family

5.1:- Who can be covered in a Family Floater Plan?

- In a family floater plan the following individuals can be covered:

- Self

- Spouse

- Children below the age of 25.

- Dependant Parents

- Dependant in-laws

- Dependant grandparents.

5.2:- Advantages and Disadvantages of a Family Floater Plan:

| Advantages | Disadvantages |

| Less premium Easy to Manage | Premiums may increase if the age difference is significant. Cover may be exhausted by a single individual. No customization. |

6:- Super Top-Up Health Insurance

- Super Top-ups or Top-ups are needed in a health insurance plan to provide additional financial aid if the base sum assured is exhausted.

- In simple words, a super top-up is a new health insurance policy that is cheaper than your original policy and has the benefit of the original sum assured and the sum assured in the new policy.

- The Top-up or Super Top-up policy is taken in addition to the base policy,

- The premium for the Super Top-up can be as low as 70% of the base premium for a much higher sum assured.

- These Top-ups generally cover the bills of hospitalization and have limited features.

6.1:- What are Deductible in Health Insurance?

The concept of deductible is particularly important to understand the ‘Top-up’ concept. It is the amount payable after which the Top-up or super top-up policy will start. This amount can be paid by you or the base policy of health insurance.

6.2:- Top-up Insurance policy

The Top-up policy pays the extra amount if every bill exceeds the deductible amount in a policy year.

6.3:- Super top-up Insurance policy

The Extra amount is paid by the Super Top-up policy even if every bill does not reach the deductible amount individually but all bills put together exceed the deductible amount in a specific policy year.

Let’s understand this with an example:

Mr. Verma and Mr Sheikh both have a 5 Lakh policy (without restoration). Mr.Verma has a 20 Lakh Top-up while Mr. Sheikh has a 20 Lakh super Top-up health insurance. Both have a 5 lakh deductible option. Both have multiple claims over 5 Lakh in the same year.

| Sr. No | Claims | Mr. Verma (Top-up) | Mr. Sheikh (Super Top-up) |

| 1 | 3 Lakh | 3 Lakh paid via base policy | 3 Lakh paid via base policy |

| 2 | 4 Lakh | 2 Lakh paid via base policy and 2 lakh paid by Mr. Verma (Top-up policy will not activate as bill amount is less than deductible) | 2 Lakh paid by base policy and 2 lakh paid by Super Top-up policy. |

| 3 | 6 Lakh | 5 Lakh paid by Mr. Verma and 1 Lakh paid by super top-up policy | 6 Lakh will be paid by the Super Top-up Policy |

Suppose you pay a premium of Rs. 24000/annum for a health insurance policy of Rs. 10 Lakh. You can get a Super Top-up of Rs. 40 lakh for an additional premium of Rs. 8000. These prices are for example purposes only and can vary.

7:- Deductibles and Non-Deductibles in Health Policy

- Deductible is a concept that was introduced by the Super Top Policies but nowadays it can be added to the base policy as well.

- It is somewhat similar to the co-pay option. The only difference is that the individual gets to choose how much deductible he/she wants in the policy.

- Suppose you have a policy of Rs. 5 Lakh and choose to opt for a deductible of Rs. 1 Lakh. This reduces your premium by a significant amount.

You had to claim Rs 4 Lakh. In this case, the insurance company will pay 3 Lakh only after you pay the initial 1 Lakh.

7.1:- Should you take a Deductible in your Health Insurance Plan?

We recommend that you do not go for a deductible in your base insurance plan. Instead, opt for a deductible in the Super Top-up Plan.

Let’s understand this with a specific example;

You buy a base health insurance plan for your family. The cover is for ₹ 10 Lakhs at an annual premium of ₹24,000. On top of this, you take a Super Top-up of ₹50 Lakhs with a deductible of ₹10 Lakh at an annual premium of ₹8000. This way you save a lot on the premium and get additional financial coverage.

If you had gone for a Normal Health insurance plan of ₹ 60 Lakh coverage, the premium would have been way higher than ₹32000/annum.

8:- List of Blacklisted Hospitals for Health Insurance

- Blacklisted Hospitals are a big NO for any insurance companies. These hospitals have been particularly chosen as Blacklisted due to fraudulent insurance claims, bad standards, failed audits, etc.

- You should be aware that if you get yourself admitted to a Blacklisted hospital you are not going to get any sort of claims.

- For each company, the list may be different, so make sure you go through that list. Never get admitted to any of the hospitals mentioned in the list.

- You can check the list of blacklisted colleges from this list:- CLICK HERE.

9:- Conclusion

As Seafarers, it is of paramount importance that we make effective and informed decisions when it comes to choosing a Health Insurance policy for ourselves and our family. In case of an emergency, you may be sailing somewhere in the mid-Pacific. Your Family should not go through any financial turmoil during this period.

10:- Frequently asked questions about Life Insurance.

- If you have savings, is health insurance still important?

- Yes, health insurance is particularly important to safeguard your assets and let the magic of compounding take its positive toll on your financial wealth.

- Top 3 add-ons that can make your health insurance a smart decision?

- 3 add-ons that should be must in a good health insurance are: (1) Higher No Claim Bonus, (2) Free Annual Health Checkups, (3) Alternative Treatments(AYUSH).

- What essential daycare treatments should a good policy cover?

- Chemotherapy, Dialysis, Appendectomy, Stone removal, and Radiotherapy are some of the essential treatments that a good policy should cover.

- What are some of the Essential Tests that a Free Health Checkup must include?

- CBC or Complete Blood count, Lipid Profile, Cholesterol & Urine Analysis are the essential tests that a free health checkup must include.

- When is the best time to buy Health Insurance?

- The best time to buy health insurance should ideally be in your 20s as you are the most healthy and have to pay the lowest premiums.

- You should buy a health insurance policy for yourself and your family as early as possible.

- Are Maternity benefits and newborn children covered in family floater plans?

- Generally, a family floater plan with maternity benefits covers the newborn child only after 90 days. However, some policies are coming up that cover maternity-related costs and any pre/post-natal complications from day 1. Read the terms carefully.

Disclaimer :- The opinions expressed in this article belong solely to the author and may not necessarily reflect those of Merchant Navy Decoded. We cannot guarantee the accuracy of the information provided and disclaim any responsibility for it. Data and visuals used are sourced from publicly available information and may not be authenticated by any regulatory body. Reviews and comments appearing on our blogs represent the opinions of individuals and do not necessarily reflect the views of Merchant Navy Decoded. We are not responsible for any loss or damage resulting from reliance on these reviews or comments.

Reproduction, copying, sharing, or use of the article or images in any form is strictly prohibited without prior permission from both the author and Merchant Navy Decoded.